3 min read

NCS Credit’s Lien Index Ends Q4 2024 at 57, Down 7% from Q3

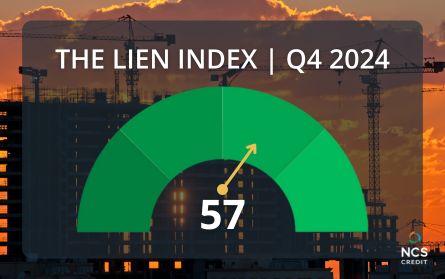

Slow payments continue to plague the industry, as the Lien Index ended 2024 at 57. Upside: lien activity did slow in Q4, with 4 point drop from Q3.

National Mechanic’s Lien Activity

The Lien Index ended 2024 at 57. This is an approximate 7% decline in activity from Q3 2024 and 5% decline compared to Q4 2023. Even though activity has slowed, lien activity remains above 50, as payment issues persist on projects nationwide.

The Index is predicted to remain over 50 in 2025, as we brace for a likely increase in bankruptcy filings and potential changes in corporate taxes, tariffs, and infrastructure investments.

Regional Mechanic’s Lien Activity

The South consistently led the nation in lien activity throughout much of 2024. However, in Q4, lien activity dropped sharply by 15%, yet remained well above 50, as lien filings continue.

In the Northeast, lien activity decreased by 10%, while the Midwest saw a 4% decline. After a couple flat quarters, lien activity in the West jumped 6% over Q2/3 and a significant 13% over Q4 23.

States with Highest Lien Activity

The top 5 states for lien activity were (in order of volume): Texas, Florida, California, Nevada and New York.

Top 3 States by Region

- West: California, Nevada, Colorado

- Midwest: Iowa, Ohio, Illinois

- South: Texas, Florida, Georgia

- Northeast: New York, Massachusetts, New Jersey

Looking Forward

As we navigate 2025, payment issues will continue to impact businesses throughout the supply chain, from material suppliers to contractors. Delayed payments and cash flow shortages continue to create significant financial strain, with slow-paying customers and financially troubled creditors compounding the pressure. The ripple effect is spurring uncertainty across the industry.

That said, contractor confidence remains strong, driven by ongoing demand in construction and infrastructure. Unfortunately, the economic outlook is still volatile. Bankruptcy filings are projected to rise, which will only increase the risk of unpaid bills and potential losses. In addition, shifts in taxes, tariffs, and infrastructure policies could introduce new challenges, or opportunities, depending on how the landscape evolves.

In this environment, it’s critical for businesses to be proactive in protecting their financial interests. Mechanic’s liens and UCC filings are powerful tools that give you legal recourse in case of non-payment. These protections ensure, even in uncertain times, your business has a clear path to securing payment for the work you’ve done. Take action now to safeguard your business against the challenges ahead.

Industry Experts

The Architecture Billings Index (ABI) dropped significantly in December, despite better conditions earlier in the Q4. “Firm billings have now decreased for the majority of firms every month except two since October 2022. While not a full-fledged recession, this period of softness and uncertainty has been challenging for many firms. And prospects for future work remain soft as well. Although inquiries into new projects continued to increase at a relatively slow rate, the value of newly signed design contracts decreased further in December as clients remained hesitant to commit to new work. In one brighter spot, backlogs at firms remained steady and strong at 6.5 months in December, so many firms still have work in the pipeline for now.” – The December ABI report

Associated Builders and Contractors (ABC) reported its Backlog Indicator was down to 8.3 months in December. “While backlog inched lower in December, contractors broadly expect construction activity to pick up in the first half of this year,” said ABC Chief Economist Anirban Basu. “Contractor confidence remained extraordinarily elevated in December, with the share of contractors that expect their sales to increase over the next six months now at the highest level since early 2022. Despite that confidence, the path of interest rates will play a critical role in industry performance in 2025. If rates remain higher for longer, backlog may remain subdued, especially in the struggling commercial and institutional category.”

The Dodge Momentum Index ended 2024 with 10.2% growth in December. “Commercial activity rebounded strongly in December, thanks to a re-acceleration in data center and warehouse planning activity,” stated Sarah Martin, Associate Director of Forecasting at Dodge Construction Network. “Overall, the strong performance of the Momentum Index this past year is expected to support nonresidential construction spending throughout 2025.”

Epiq Bankruptcy reported a 20% increase in Chapter 11 filings in calendar year 2024. “The continued increase in bankruptcies over the past year reflects the growing list of economic challenges faced by consumers and businesses,” said ABI Executive Director Amy Quackenboss. “Rising interest rates, inflation, increasing geopolitical tensions and shifts in post-pandemic consumer spending have more struggling businesses and families turning to bankruptcy for a financial fresh start from their growing debt loads.”

Healthcare Bankruptcies Are Rising: A Risk to Suppliers

Healthcare bankruptcies are up 300%+ since 2010. See what unsecured creditors really recover — and how a UCC filing changes the outcome. Free download.

Full vs. Unpaid Balance Lien States Explained

Learn how full price and unpaid balance lien states affect your mechanic's lien rights as a subcontractor or supplier - and how to protect them.

Mechanic's Lien Recovery by State: Full Balance vs. Unpaid Balance

Download this resource to see which states are full pay vs. unpaid balance lien states, and learn why timing your mechanic's lien filing matters.